SpaceX is going public at $135 a share, seeking a valuation of $1.75 trillion. Newscasts talk about colonizing Mars. Investment forums burn with promises of quick wealth. I, however, look at the financial statements.

Economics is logical, sometimes. And logic dictates that buying promises at astronomical prices is speculation, not investing. And I do not mean by this that speculation is all bad, quite the contrary! I have carefully read the data leading up to the SpaceX IPO. I have analyzed their cash flows. Applying my principles, the current ones. Those taught to me by the Austrian School and Value Investing, let's dissect this operation.

The Mirage of EBITDA and the Reality of FCF

The market celebrates the $18.67 billion in 2025 revenue and an adjusted EBITDA of $6.58 billion. But EBITDA assumes the tooth fairy pays for capital expenditures. SpaceX is a shredder of physical capital.

Building Starship, deploying massive satellite constellations, and standing up AI clusters requires steel, titanium, servers, and thousands of engineering hours. Those are real costs. The company reported a GAAP net loss of $4.94 billion in 2025.

For a programmer, think of it this way: using EBITDA to value a business is like measuring your application's performance while ignoring the cost of cloud infrastructure. You think you are profitable because your code compiles quickly and attracts users, but AWS is ruining you at the end of the month. The real metric is Free Cash Flow (FCF). And SpaceX's FCF, dragged down by over $3 billion in R&D for Starship alone, is deeply negative.

Structural Moats: The Cost per Kilogram

Do not misunderstand me. The company possesses real competitive advantages, what we call an Economic Moat. Its cost advantage in the Space division is overwhelming. They have turned access to low Earth orbit into a commodity dominated by their reusability technology.

Technically, their durable competitive advantage is not the physical rocket, but the data feedback loop they have built. Each landing trains their predictive models, reducing wear and inspection time. It is an insurmountable physical network effect. Furthermore, Starlink acts as a layer 1 connectivity provider where the switching cost for enterprise clients is immense. Integrating military systems or shipping fleets with Starlink's APIs requires months of development. Once the client is in, the cost of leaving is prohibitive.

Possessing a moat protects you from competition. But it does not protect you from paying an irrational price.

Fair Price vs. Announced Price

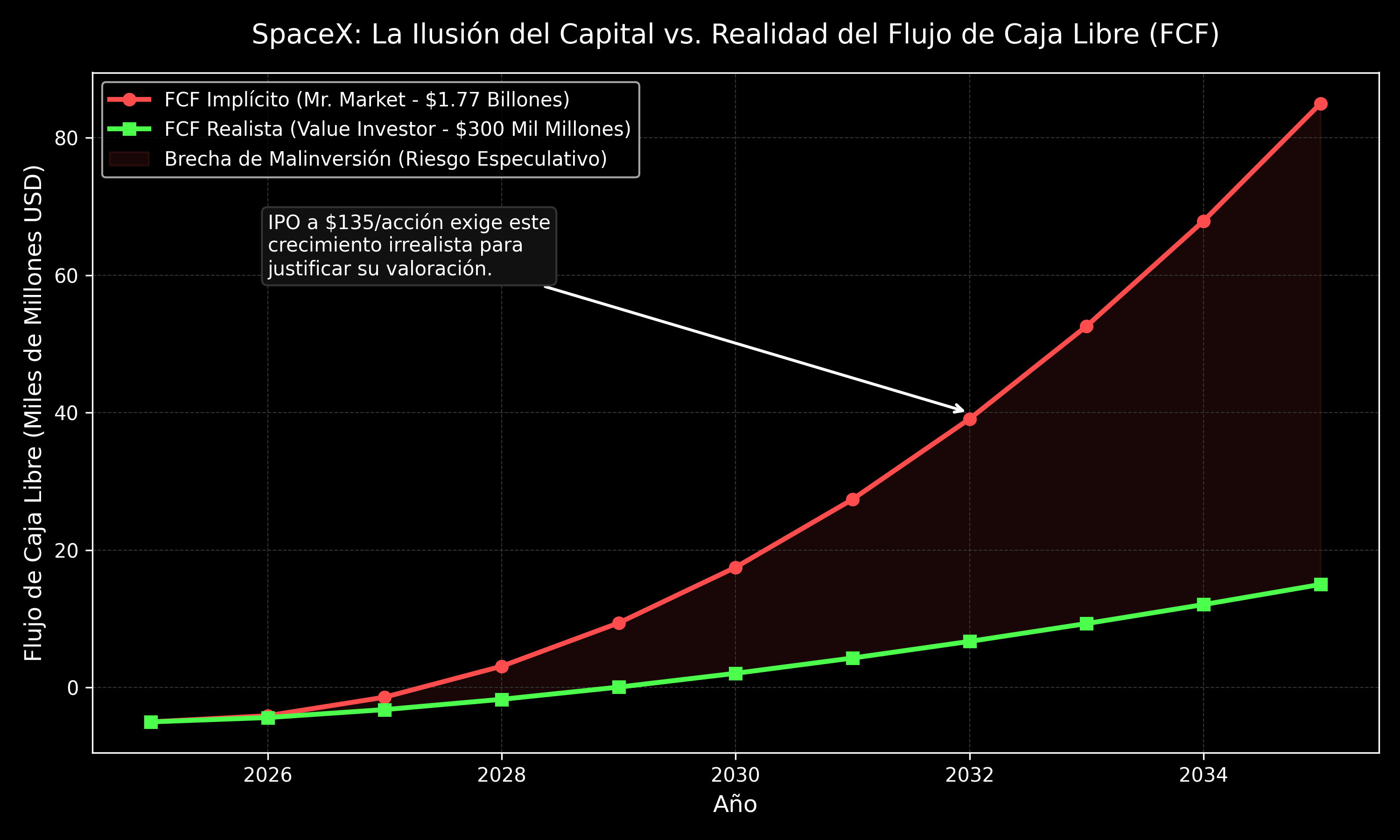

The $1.77 trillion valuation requires believing in miracles. It demands that we project perfect and growing cash flows over the next twenty years, discounted at an artificially low interest rate.

Let's reverse engineer this. To justify $1.77 trillion with a minimum required return of 10% (Opportunity Cost), the company would need to generate tens of billions of dollars in annual FCF in its mature stage. In 2025, its most profitable segment (Starlink) had an operating income of $4.4 billion. The gap between today's operational reality and future expectations is an unbridgeable abyss.

Based on a severe discounted cash flow analysis, isolating the Starlink business (the real cash engine) and assigning a modest residual value to the launch business, SpaceX's intrinsic value hovers, being generous, around $300 billion to $400 billion. Demanding a 40% margin of safety against the Knightian Uncertainty of space exploration and artificial intelligence clusters, the fair price of the stock oscillates between $20 and $25. Never $135.

Paying $135 is speculating. It is acting with an extremely high time preference, hoping that mass psychology validates the multiple and buys it from you at a higher price tomorrow.

Expected Evolution: From Boom to Re-coordination

What can we expect from this stock?

- Short Term: The price will likely rise. Liquidity will push the shares up, driven by the fear of missing out (FOMO) and the stellar narrative. We will see headlines celebrating the greatest success in financial history. Speculators will make nominal money benefiting from the Cantillon effect, assuming a destructive asymmetric risk.

- Medio Term: The correction will come. When real interest rate hikes strangle credit and cost inflation hits industrial prices, the market will demand to see real cash, not projections. The fade rate will act mercilessly. The price will collapse to re-coordinate with the real value of cash flows, purging the malinvestment.

- Long Term: SpaceX will survive the cull. Its moats in orbital logistics and communications are solid. Those who have the coldness to buy the remnants of euphoria during the inevitable market panic, acquiring stakes at $20, will obtain formidable compounded returns.

The market gives away nothing. Let others pay for the $135 party for the Martian dream. We will keep our liquidity ready, and wait to buy the company with a margin of safety.

Operative Annex: The Discipline of the Short-Term Speculator

If you decide to temporarily abandon productive investing to arbitrage mass psychology on the first day of trading, you must do so with military discipline. Playing musical chairs with a stock that IPOs at $135 demands not being the exit liquidity for large institutional funds.

- The Opening Trap: Never launch a "Market Order" at the open. The crosses are chaotic and your broker will execute the order at the absolute peak of initial euphoria (e.g., $210), leaving you instantly trapped.

- The Defensive Entry: Enter a Limit Order at a maximum of $145 - $148. You agree to pay a small toll over the IPO price to enter the FOMO inertia, but you protect yourself from buying at the absolute top. If the stock opens directly at $180, your order is not executed and you protect your capital.

- The Scaled Exit (Take Profit): The artificial scarcity of the first day (very low free float versus global demand) usually forces a pop of 30% to 45%. Scale your exit beforehand: set sell orders to unload 50% of the position at $175 and the rest near $190. Lock in the capital gain and let someone else assume the risk of reversion.

- The Firewall (Stop Loss): If the market rejects the valuation and falls, the psychological support of $135 breaks. Place a strict Stop Loss at $124 to avoid getting trapped in a prolonged malinvestment. Cut losses without emotional attachment; remember that sunk costs are irrelevant.