If there is a recurring debate in economic policy, it is the relationship between new housing construction and its price. The short and direct answer to the question is yes. Classical market theory doesn't fail: if you increase supply above demand, the price drops. Spain's problem is not that building doesn't lower the price, but rather that in reality almost nothing is being built in proportion to the tsunami of demand, and the State systematically prevents private initiative from scaling production.

The supply curve versus historical data

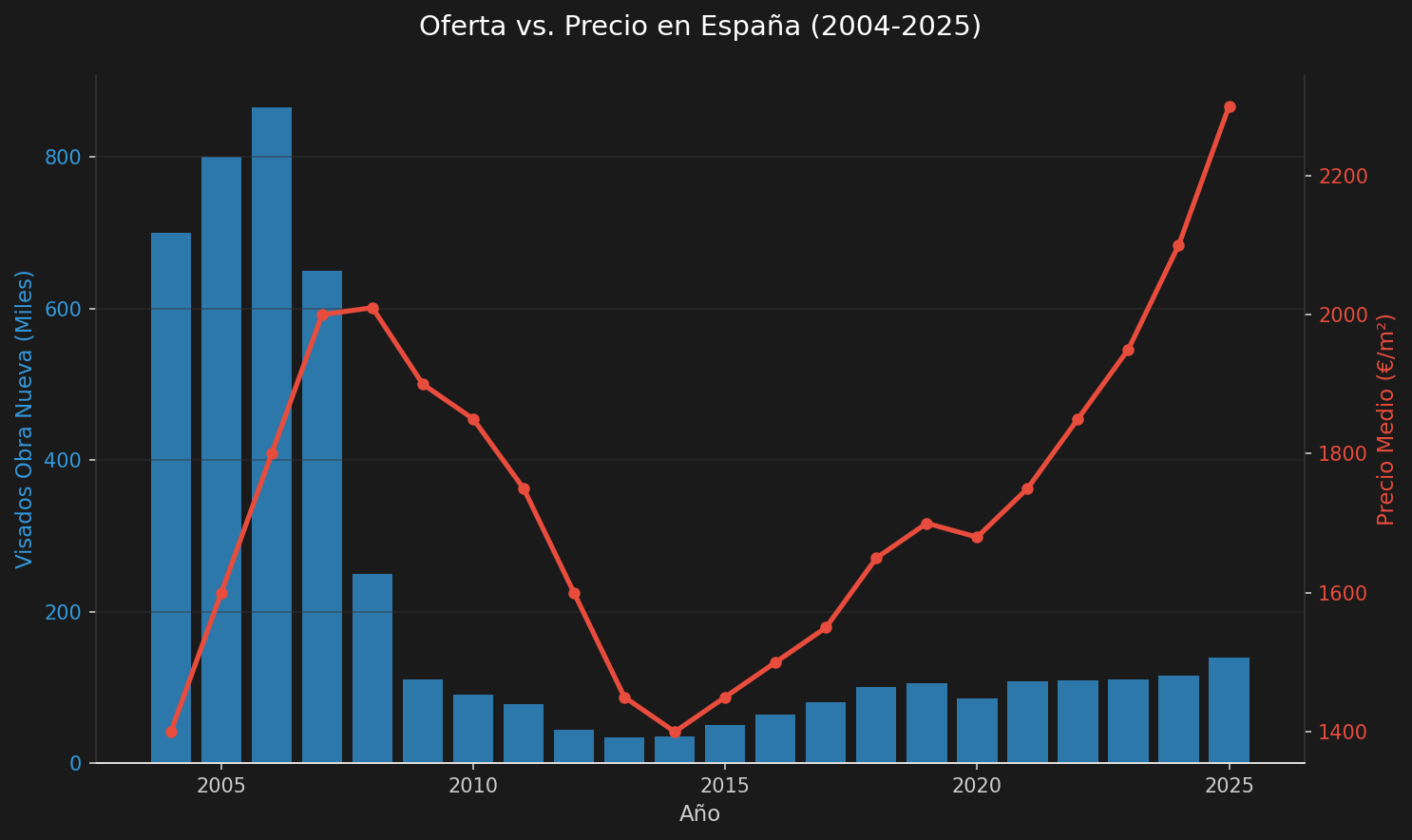

I have consolidated the data from the last two decades in Spain using historical series from the Ministry of Housing and Urban Agenda (MIVAU) and the National Statistics Institute (INE). On the one hand, the evolution of new construction direction visas (the main metric for future production) and, on the other, the Housing Price Index (IPV).

As seen in the chart, we come from an anomalous peak in production between 2004 and 2007, where the sector exceeded 800,000 annual visas (MIVAU data). After the financial collapse, residential development hit rock bottom around 2013, with barely 34,000 visas. Since then, the machinery has started up again very slowly, bordering on 140,000 annual units in 2025.

At first glance, the supply curve is recovering, but the INE price curve maintains an uninterrupted upward slope since 2014. Does this mean that supply doesn't curb prices? No, it means that the scale of supply is completely insufficient compared to the size of the market.

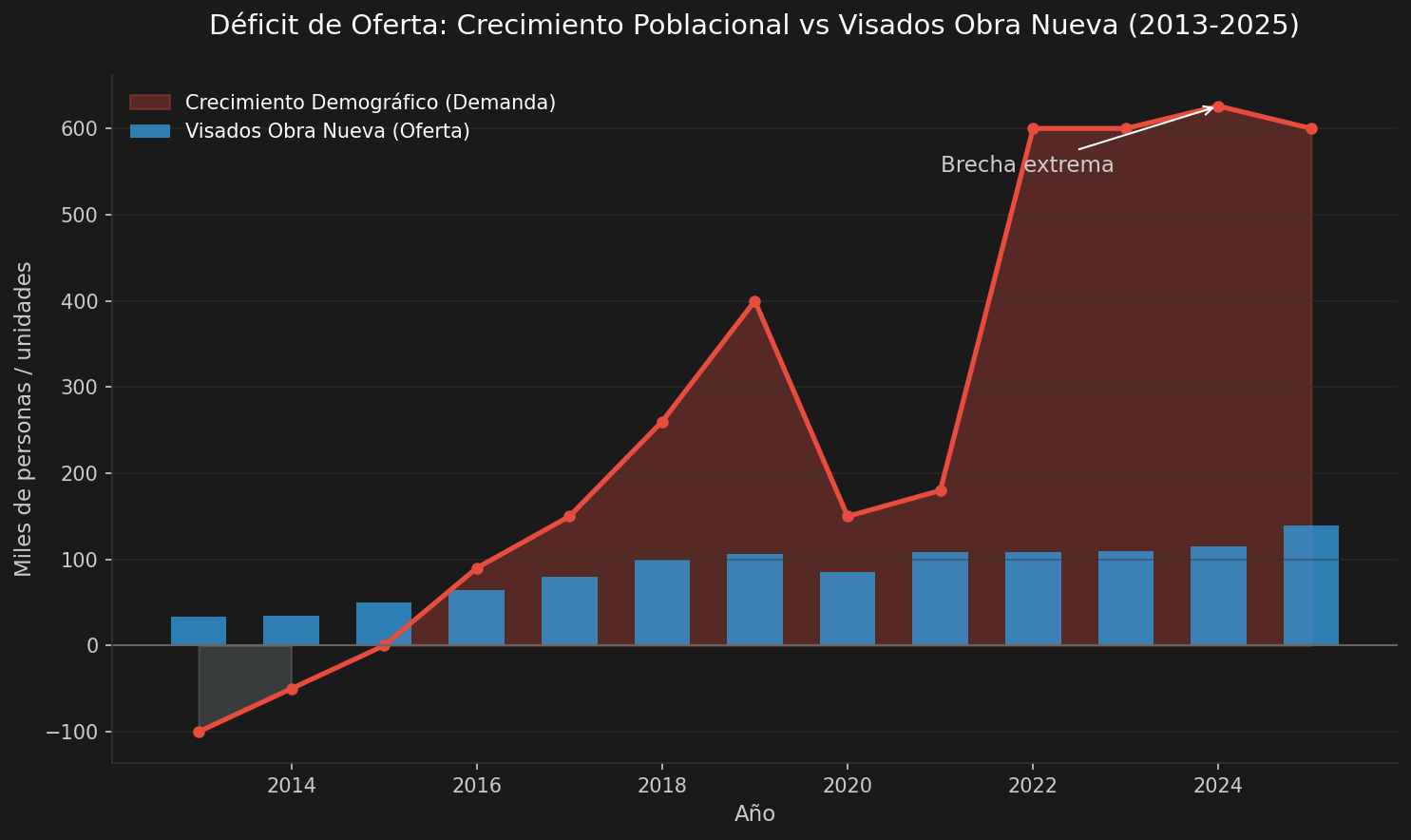

In fact, in its recent 2024 and 2025 updates, the Bank of Spain has estimated an accumulated deficit of some 700,000 homes needed just to balance the net creation of households in these past few years.

The demographic mismatch and the production deficit

Building homes does not work under an abstract model; it crashes against physical and operational barriers. There are severe market inefficiencies, artificially generated, that strangle production:

- The brutal demographic impact (The real scale). Building 140,000 homes a year sounds like a lot until we cross the data with the INE's Continuous Population Statistics. Just during 2023 and 2024, Spain registered a positive external migratory balance exceeding 600,000 people annually, pushing the population above 49.6 million at the beginning of 2026.

As this second chart shows, the huge influx of population generates an immediate demand that evaporates the precarious new supply. We don't build "a lot"; the deficit estimated by the Bank of Spain is the mathematical proof that current production is a drop in the demographic ocean.

-

Real production costs and regulatory asphyxiation. Building costs real money. According to the MIVAU's sector indices, the Material Execution Cost (CEM) has experienced drastic increases. Today it is complex to build below 1,200-1,500 €/m². The inflation of materials, the energy crisis and the new technical efficiency regulations (which raise construction standards) structurally make building more expensive. If we add to this the extremely high tax burden at each phase (licenses, ICIO, VAT, AJD) and the years of municipal bureaucratic delay (which skyrocket financial costs), the State de facto imposes a cost floor that makes it unfeasible to sell cheaper.

-

Geographical heterogeneity and effective demand. The housing market is not single, it is hyper-local. Demographic pressure is not distributed equally, but is aggressively concentrated in Madrid, Barcelona, Valencia, Alicante or Malaga. Building homes in areas without economic dynamism does not lower the price in the poles of labor attraction. In addition, we must understand the behavior of demand: the large demographic flow exerts an initial and intensive pressure on the rental and flat-sharing market (many immigrants do not immediately access buying), which explains the meteoric rise in rents in these urban environments.

-

Legal insecurity and the failure of price controls. Instead of facilitating investment in these stressed areas, punitive regulations retract the market. The case of Catalonia (data from portals like Idealista) is the greatest non-partisan evidence: the application of rental price controls has caused a drastic drop of more than 40% in the supply of regular housing, massively shifting properties to seasonal rentals and toughening requirements for tenants.

The hidden impact: The stagnation of real wages

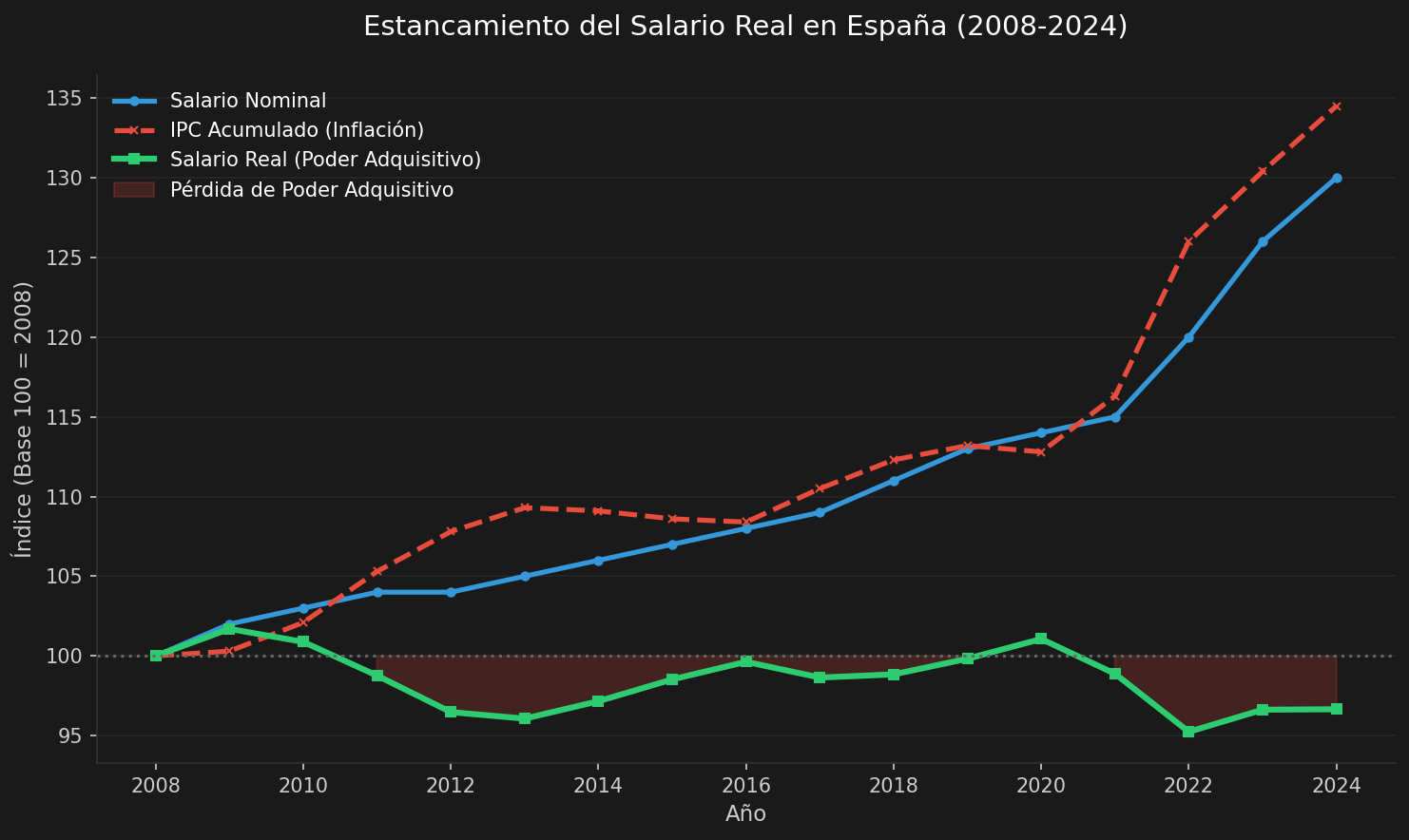

In addition to supply rigidities, there is a factor that lethally aggravates the effort required to access housing: the loss of purchasing power. Even if we managed to multiply supply, a significant part of the population would still have severe access difficulties due to the stagnation of their disposable income.

As reports from the OECD and the INE reflect, the average nominal wage has risen (partly driven by the continuous increases in the Minimum Interprofessional Wage), but the brutal accumulated inflation has eaten up that rise. In terms of real wages (purchasing power), the youth and Spanish middle classes are poorer today than fifteen years ago. Wage compression means that the financial effort to pay for the square meter is increasingly greater.

Structural solutions beyond "building more"

The base resource, land, is hyper-regulated. The land on which it is legal to build is rationed by the administration, creating an artificial shortage that skyrockets prices. For the increase in supply to have a real impact on prices and for the market to absorb that deficit of 700,000 homes, it is necessary to liberalize the market through forceful solutions. It should be clarified that liberalizing urban planning to absorb genuine housing demand has nothing to do with the credit boom of the 2004-2007 bubble, which was doped by the injection of cheap money and easy credit without risk control. The real structural solutions lie in:

- Drastically speeding up license timeframes: Licenses and land rezoning are today one of the toughest bottlenecks. Replacing this bureaucracy with responsible declarations would allow supply to be injected into the market elastically and quickly.

- Selectively liberalizing the use of buildable land: Especially in well-connected peripheries and smart densification environments. This does not imply "savage urbanism", but maintaining high urban quality standards while eliminating the artificial shortage generated by excessive and purely political regulation.

- Reducing regulatory and fiscal hurdles: Eliminating the multiple taxation that burdens real estate development and softening non-essential regulations that raise the marginal cost of construction.

- Full legal security: Unconditionally protecting private property against squatting and defaults so that risk disappears and the immense stock of empty housing naturally surfaces in the rental market, immediately relieving the tension of effective demand.

In short, construction does lower the price. What is impossible is for prices to drop in a country that attracts half a million new inhabitants a year, while the State impoverishes its citizens with inflation, prohibits using the land, chokes production with taxes and generates legal insecurity. The solution is not to control the market, but to let private initiative build and operate at the real scale society demands.